The energy crisis caused by the war against Iran is no longer confined to the Gulf. It now extends to countries far removed from military theatre, where the threat does not always take the form of a total rupture, but of a cocktail of tensions: partially dry stations, rationing electricity, more expensive freight, air fuel under pressure and high pump prices. The market remains under high pressure. On Thursday, 26 March, the Brent increased over $104 per barrel and the WTI at around $92, while investors continued to doubt a rapid relaxation in the Middle East.

The heart of the shock remains the Strait of Ormuz. Barclays estimates that a prolonged disruption of this passage could reduce 13 to 14 million barrels per day to the world market, for a global demand estimated by the International Energy Agency around 104 to 105 million barrels per day. This risk alone is enough to raise the price of crude oil, maritime insurance and logistical costs, even before the shortage appears in the motorists’ tanks.

What has changed in recent days is the geography of the crisis. The problem is no longer that of the major importers in Asia or the Gulf countries directly exposed. It now has more fragile economies, with few reserves, few budget margins and strong dependence on imported fuels. In these countries, the oil shock is almost immediately transmitted to transport, electricity, fishing, aviation or public finances.

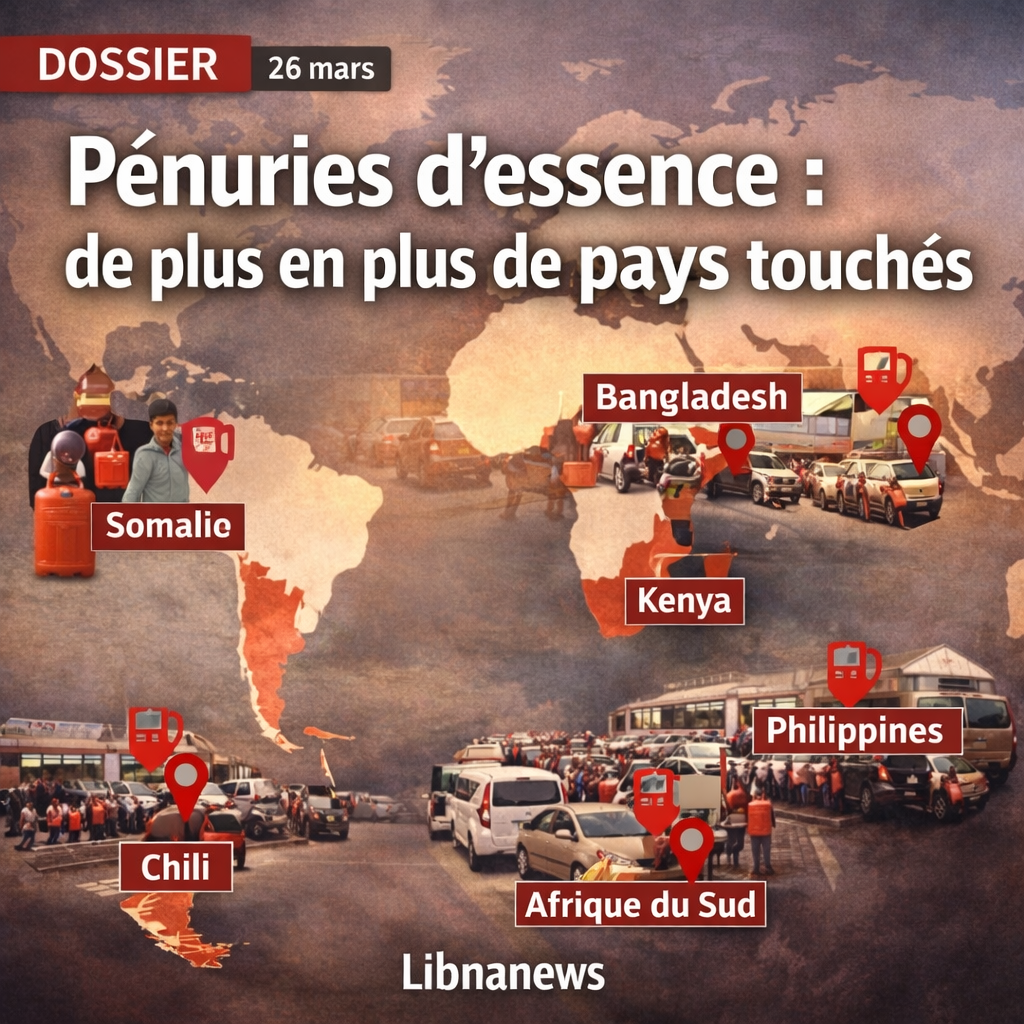

Africa on the front line

East Africa and the Indian Ocean are among the most exposed areas. In Somalia, rising fuel prices have already disrupted part of urban transport. Reuters reports that in some areas the price of fuel has more than doubled, causing tuk-tuk drivers to immobilize their vehicles because they could not cover their costs. In a country already weakened by drought and hunger, the energy crisis becomes an immediate social crisis.

In Mauritius, tension takes another form. The authorities restricted certain non-essential uses of electricity due to a lack of heavy fuel oil, pending an expected replacement load from Singapore. In South Sudan, Juba began to ration electricity. In Uganda, authorities have reported limited stocks of petrol and diesel and are looking for alternative supply routes. In Kenya, about 20 per cent of stations would face delivery difficulties, even if the government claimed that it had sufficient stocks and accused precaution purchases of increasing tension. Finally, in South Africa, localized shortages of diesel have been observed, linked to massive preventive purchases of large consumers such as farmers.

These African cases show how quickly a distant geopolitical shock becomes a daily crisis. In economies where road transport, generators and imports weigh heavily, every increase in diesel is very quickly reflected in food prices, urban travel and economic activity. The shortage does not need to be total to produce its effects. Sufficient stocks, delayed deliveries and a sharp increase in the price per litre are enough to stop the machine.

In Asia, the threat extends from kerosene to diesel

Asia appears as the other major source of vulnerability. In the Philippines, the President publicly acknowledged that a « real possibility » was an aircraft shutdown due to lack of air fuel. Several countries reported to Philippine companies that they would not be able to provide supplies, forcing some of them to board enough fuel for the round trip. The problem therefore exceeds the price of oil alone: it already affects international air transport logistics.

Bangladesh is seeking more than $2 billion in external financing to secure imports of liquefied natural gas and fuel. The country depends on 95 per cent of imports for its energy and is already using rationing measures, although some have been temporarily relaxed during Eid. Dhaka negotiates with the IMF, the World Bank, AfDB and other donors to avoid a break in energy financing. That says a lot of the gravity of the moment: for some States, the priority is already no longer just to amortize prices, but to find the necessary dollars to continue to buy.

Other Asian countries are not yet talking about a widespread shortage, but about a shock that is severe enough to trigger emergency measures. In Thailand, the fishing industry is approaching closure. More than half of the trawlers at Samut Sakhon’s main fishing port remain at dockside, with diesel increasing from 29.94 baht per litre in February to 38.94 baht on 26 March. The government is preparing support, and the Department of Finance is also examining a reduction in fuel tax to curb pump price increases.

South Korea has also activated the emergency arsenal. Seoul announced a debt buyback to support liquidity, but above all an increase in gasoline and diesel tax relief, as well as an unprecedented cap on domestic fuel prices. The government also wants to increase nuclear production and relax certain restrictions on coal in order to contain the energy shock. This shows that even in a developed and industrialized economy, oil spills and the closure of Ormuz require an immediate response.

Beyond these examples, the Associated Press describes an entire region in defensive mode: India is reviewing its supply priorities, Pakistan is limiting certain uses, Nepal is rationing the GPL, and several governments are seeking priority protection of basic needs. In Asia, therefore, the crisis is measured not only at the price of the barrel, but at how each state prioritizes access to energy between households, transport, industry and aviation.

In Latin America and Europe, the shock becomes political

Chile offers one of the most spectacular cases of direct pump transmission. As of 26 March, petrol at 93 octanes is expected to increase by about 370 pesos per litre in Santiago, around 30%, while diesel increases by about 580 pesos, or nearly 60%. The government activated a clause in its fuel stabilization mechanism to quickly realign domestic prices to world prices, believing that it could no longer finance the budget shield indefinitely. According to the authorities, absorbing the entire shock would cost up to $4 billion.

In Europe, the answers remain more cautious, but political pressure is rising. In Germany, Chancellor Friedrich Merz acknowledged that public finances could not compensate for all the increases associated with the war against Iran. Berlin is thinking about targeted relief devices, but refuses the idea of an unlimited shock absorber. In Austria, the lower house of Parliament approved a text opening the way for measures to reduce taxes and margins on petrol and diesel, with the stated aim of reducing prices by about 10 cents per litre from next month.

This difference in tone between Berlin and Vienna is revealing. Some governments already admit that they will not be able to absorb everything. Others are still trying to slow down the transmission of the shock to the final consumer. But in both cases, the signal is the same: fuel becomes again a major social and budgetary subject, as in 2022, this time with often narrower public margins and inflation that threatens to return.

Why the risk of shortage is not limited to empty stations

The term shortage can be misleading. In some countries, it already refers to local supply disruptions. In others, it refers instead to a relative shortage: fuel more difficult to find, queues, precaution purchases, rationing of electricity or prioritisation of uses. The case of Bahrain, the Gulf or large Asian economies recalls that a system can still work while being deeply weakened by explosive logistical costs and more uncertain supply delays.

What worries most is not only the absence of gasoline today. It’s the duration of the shock. Markets remain convinced that regional security will not be restored quickly. Reuters notes that oil jumped dramatically over the month of March and that European gas also rose sharply, fuelling fears of a return to inflation and increased pressure on interest rates. The longer the crisis lasts, the more it is passed on to the whole chain: road transport, agriculture, fisheries, sea freight, aviation, electricity generation and public budgets.

In the most vulnerable countries, this can quickly become a balance of payments crisis. In richer economies, the risk is less that of an immediate dry breakdown than of a lasting increase in daily life. In all cases, gasoline and diesel again become a direct indicator of global vulnerability to regional war.

A list of countries that continue to expand

At this stage, the most clearly documented cases include Somalia, Mauritius, South Sudan, Uganda, Kenya and South Africa in Africa; Philippines, Bangladesh, Thailand and South Korea in Asia; Chile in Latin America; as well as Germany and Austria in Europe, where the question arises mainly in terms of prices and public support. Depending on the country, these are localized shortages, tight stocks, energy rationing or already politically explosive price increases.

The current sequence recalls a simple reality: a war against Iran not only produces a geopolitical or stock market shock. It places gasoline, diesel, kerosene and security of supply at the centre of global fragility. As long as the Strait of Ormuz remains under threat and markets are uncertain about a solid de-escalation, the question will no longer be that of the price of the barrel, but of which countries will have the financial, logistical and political means to hold longer than others.